After almost a year, I’m back on the blog. Heading into the third pandemic-affected filing season, much has changed here at Tax Therapy.

First, I am working from home for the foreseeable future. That means the practice has transitioned from mostly office-based to mostly virtual. The only clients I will be seeing in person are those who qualify for a house call. I am still taking paper documents through the mail or, if you are in the Albuquerque area, by local courier. If you are a potential client please continue to browse the website and then, if you feel like I can meet your return preparation needs, click here to book a discovery call.

Second, I am (for the most part) now working solo. Cat has a new full-time job and will be helping as necessary to wrangle actual, and occasionally electronic, documents, but she will not be here to provide near instant answers to your phone calls and e-mails. Please allow 24-48 hours for a response and understand that during March it can take me up to 72 hours to respond to your inquiries.

Third, while I am currently accepting new clients, I am only accepting new 1040 clients (individual returns). I will not accept new clients who require entity returns (Forms 1065 or 1120-S) once filing season has started. Entity returns are much more complicated and the new client onboarding process is much too involved for one person working alone to attempt during tax season. Entity returns also have a March 15th deadline and I don’t feel that I can realistically meet that deadline for entity clients who are brand new in January. If you are interested in having me prepare your entity return, I encourage you to use the contact form to let me know and I will put you on a list of potential clients to contact later this year (typically starting in June).

Finally, my cutoff date for accepting new clients will likely be even earlier this year than it was last year. Last year I stopped accepting new clients on March 10th. This year I expect to stop accepting new clients as early as February 20th to ensure that I can manage my workload and meet the April 18th filing deadline for as many clients as possible. I have not yet decided whether or not I will be taking new clients during the summer and fall extension period. As Magic 8-ball says “signs point to no” but I reserve the right to change my mind.

Everyone (the IRS, the National Taxpayer Advocate, tax industry organizations, and tax professionals) are predicting another “hairy” filing season. Personally, I’m feeling a return to something resembling normal but I am also preparing for a bumpy ride. So put on your seatbelts and let’s get going!

1972 Mercedes in the Nevada desert.

And not all tax people are interchangeable.

This is my Dad’s car. Imagine that this car is having an, as yet unidentified, engine problem. Here’s a short list of items that make this car special:

- It’s old

- It’s foreign (specifically German as opposed to Japanese)

- It’s considered a “performance” or “sports” car

- It was manufactured for sale in 1970s California (in other words, specialized emissions equipment)

My dad lives in a town with maybe one professional mechanic and a lot of hobby mechanics. Many of the hobby mechanics are pretty good mechanics, at least when it comes to cars they know. Many of the hobby mechanics have access to the internet and are willing to do their research and ask other mechanics questions. So, what’s the best option here? Put this classic car into the hands of a hobby mechanic? Take it to the local pro who works mostly on Fords and Toyotas? Or actually get it on a trailer and take it to someone who is a recognized specialist in this type of car? Maybe someone who was trained by someone who was a mechanic in California in the 1970s and who now specializes in vintage German cars? I guess it depends on how much you value your money, your time, and your car.

What does this have to do with taxes you ask? Well, I’m seeing a lot of hobby mechanics holding themselves out as professional mechanics and working on cars they have no business working on. Cars they can really damage but the owner won’t know it for the first several thousand miles. I’m seeing brand new tax professionals asking questions on Facebook about changing entity selections, about foreign tax issues, about complex individual and business tax planning when they are simultaneously asking questions that make it clear they don’t understand the difference between federal income tax withholding and FICA withholding. It’s as a friend of mine put it “horrifying.”

Even professional mechanics don’t know everything about every car. It is the same with #taxpros. Those who specialize are great at what they do but may only have a basic knowledge of other areas that also may require specialization. Understand that when you are shopping for a professional to prepare your return you may be getting a hobby mechanic instead of a professional mechanic. You may be getting a professional mechanic (#taxpro) who specializes in Ford F-150s instead of vintage, foreign, diesel engines and your car (tax return) is a 1971 Peugeot diesel. Maybe the mechanic can work on your car but should the mechanic work on your car or refer you to the specialist across town? One hopes an ethical mechanic will either decide the problem is only slightly outside their scope of competence and they have resources (other mechanics and the internet) with whom they can consult or send you on down the road. But what if they don’t? What if by the time you find out that your engine is damaged (that you’ve received the first IRS notice) you are already looking at sinking quite a bit of time and money into undoing the damage? What if indeed.

If you wouldn’t turn your car over to a hobby mechanic, why are you shopping for a #taxpro based on price, fast turnaround, and/or location?

When it comes to hiring someone to “do your taxes” choose wisely. The consequences of failure can be high (and expensive).

Read more about How to Choose a Tax Professional here.

A couple of weeks ago I was talking with some colleagues about being forced to watch videos to learn features available in new software and just how much I didn’t like that. The videos are slow. I can read faster than that and I comprehend better as well. Usually, I’m going to want to read about something and then maybe watch the video to see how it’s actually done. That’s not how I roll 100% of the time, but in general I’m a reader not a watcher.

A couple of weeks ago I was talking with some colleagues about being forced to watch videos to learn features available in new software and just how much I didn’t like that. The videos are slow. I can read faster than that and I comprehend better as well. Usually, I’m going to want to read about something and then maybe watch the video to see how it’s actually done. That’s not how I roll 100% of the time, but in general I’m a reader not a watcher.

I’m considering this in light of recent client pushback concerning my (admittedly lengthy) “help” e-mails. I’m writing volumes of free help information that targets specific issues my clients are having and distributing it to clients along with links to video help and the knowledge base provided by the software. My business is doing tax returns, not doing tech support on my client management software. That said, I want to help when different clients are all having the same or similar problems. So, I write. Why don’t I do video? Because the software has done that. Also because some people, like me, prefer written to video help. So, I’m doing my best to do both what works for the office and what allows me to “meet clients where they are” so to speak.

While the office has always been able to manage contact free service in one form or another (mail, portal, etc.) after last year I decided that we needed to automate some of the more routine administrative aspects of the return preparation process as well as to increase our “one to many” communication. The change was necessary in order to accommodate client volume while still maintaining a degree of personal service and some work life balance for the office staff (me and Cat). We want to be able to focus on tax returns and complex issues, not booking appointments or answering e-mails about the secure portal. Pushback on these changes has included clients leaving and me telling clients that we can no longer meet their expectations and to find a new preparer. Yes. I have fired clients who, instead of asking for help with a specific problem, simply wanted to complain about not liking the changes I am making—to my business.

I get it. Change is hard. No one likes it. Me included. I’m in my 50s and it’s not getting any easier for me to adapt either. But sometimes it’s adapt or die. Last year it became adapt or die for this office. The changes I’m implementing, while causing some short-term pain, will be both beneficial and necessary for the long-term future of my business. So, while it is unfortunate that some clients have chosen to leave or I have chosen to curate them from my client list, I still hope that they find another preparer who meets their needs. Specifically I hope that

- The new #taxpro pays attention to office and internet security

- The new practitioner’s business model meets both their price point and their income needs

- If the new practitioner’s business model is built on working 60-80 hour weeks during tax season (especially during this tax season which has been compressed by an additional two weeks and hundreds of pages of new tax law) that they are able to prepare the return accurately. The cognitive decline that comes from a lack of sleep is a real thing. Tired #taxpros make more mistakes.

- If the new practitioner’s business model is built on doing a high volume of returns at a low price that they spend enough time with you and on your return to prepare it accurately the first time. And if they don’t that they are around in the off season to help you with any resulting IRS or state notices.

Why do I hope this? Because high-volume, low- to mid-price business models are getting increasingly harder to sustain without automation. The Covid-19 related legislation alone is adding 20-30 minutes to each tax return I prepare just to make sure I’m getting clients all the benefits for which they may be eligible and the correct amount of stimulus money. I read about one #taxpro who says he spends his summer amending returns for free because of all the mistakes he makes during season. He works six or seven days a week and ten to fourteen hour workdays. No wonder he’s making mistakes. Then there’s the general cognitive decline that comes with age. I do not have the memory I had when I was 30. Or even 40. I’ve added automations as “brain extenders” because I’m not willing to run the risks that come with cognitive decline when those risks affect your tax returns.

Maybe you don’t care. Maybe face-to-face completely unautomated service is so important to you that you go out and find a relatively young “old school” preparer. Maybe you won’t outlive them. Maybe they won’t also decide that their business model is unsustainable and decide to make changes. Maybe the demands of the job the way they are currently doing it won’t cause them to make errors. Or maybe, just maybe, it won’t be this year and it won’t be your return.

#fullambo out

The two most beautiful words I heard on #TaxTwitter this weekend were “seller’s market.” What does that mean? It means that good #taxpros are in demand. Good #taxpros. I’m seeing loads of newbies on FaceBook who have passed a test or taken a few classes and decided to open a tax practice asking for advice on everything from what to charge to who qualifies as a dependent to, wait for it, how to prepare a Schedule C.

I’ve mentioned before that “not caught is not the same as accurately filed.” By the time taxpayers get the notices on these returns these preparers have probably closed up shop for the season and are nowhere to be found. Not all of them. Some, who decided to charge really low prices to get clients in the door, will still be working filing what I hope are free amended returns to fix their mistakes. That sucking sound you hear is their profit margins going down the toilet because they charged too little to begin with and now they have the pleasure of doing the return twice. At least I hope they aren’t charging for the amended returns. I had to call a client yesterday morning and to tell her I recently became aware of some “fine print” that could result in tax savings for her and because it was something I missed on her returns I would, once I verified my mistake was really a mistake and she qualified for this benefit, be filing three years’ worth of amended returns for her, for free. Why? Because I’m a good #taxpro. And we are in demand.

You want to know how I know we are in demand? Because the first question potential clients are asking me isn’t “How much do you charge?” it’s “Are you taking new clients?” The answer is yes, but not all of them.

Last year was hard on tax professionals. Some of us aren’t convinced “last year” ever ended. People made themselves ill, people got hives from the stress, people died, some died at their desks and here we are starting what appears to be another chaotic filing season. Last year was absolutely brutal on me and I only have a small practice and not many small business clients. I was stressed, exhausted, and angry. I’ve been working continuously since last January and I’m still stressed, exhausted, and angry. I’m just handling it better. Part of the reason I got no break was that I decided that what made the 2020 extended filing season so unsustainable was the administrative work (e-mails, phone calls, etc.) associated with scheduling appointments for potential and existing clients, answering the same questions over and over, and chasing paperwork (specifically my engagement packet and annual client interview) while trying to keep up with tax law changes and preparing tax returns. Part of the reason I’m handling the stress better is that I spent most of October through December of 2020 adding software that automates the administrative parts of return processing and appointment scheduling so that Cat and I can focus on preparing complete and accurate tax returns for our clients instead of answering the same handful of questions dozens (or hundreds) of times by phone or e-mail.

So why the salt? In a word? Pushback.

So why the salt? In a word? Pushback.

I get it. Change is hard. If you think it’s hard to adjust to a new system imagine having to actually set up the new system and use it, not just once but hundreds of times. And yet, most of my clients are managing. Even the ones I thought of as “not super techy” are giving it a try and figuring it out. It’s an imperfect system and I’m learning as I go. It’s not always easy and at times everyone has been frustrated (clients, me, Cat). I am letting the frustrated clients know that I appreciate their patience and feel their pain. I also understand that it’s harder to adapt to a new system when you only use it once or twice a year. I’m cutting some slack, but I’m not cutting slack like I did in 2020 when I basically did whatever I could to help my clients even if it meant sacrificing my own well being.

After fielding a few calls from disgruntled clients, I decided yesterday that I’m simply not taking pushback on my new client management system. My office processes are reasonably flexible and always have been. I will take what I am learning this year and make refinements that make the system and my processes easier on both the client and the office side. I don’t want to frustrate my clients, but I also don’t want to be crushed under the weight of admin work that can be automated.

Consider this, when you find a doctor that is taking new patients do you tell that doctor how to run her practice? I don’t think so. Well, when you find a tax professional, especially an ethical, competent, experienced tax professional, who is taking new clients, it’s probably a good idea to work within their systems instead of telling them how you want to do things.

If you’re reading this and thinking “Well, that’s nasty, I will just take my business elsewhere” I understand. But remember…seller’s market. I’m not trying to price gouge you. I’m not trying to make your life hard. I’m trying to earn a living in a demanding job with extremely high consequences of failure without killing myself in the process. So if my office policies and procedures don’t meet your idea of the way you think things should be done, shop around and find someone with a practice that does. It may be a seller’s market, but there will always be practitioners out there at all price points, experience, and service levels.

Clients who value me will find me and clients who don’t will find a practitioner that better meets their needs. Because truthfully, when it comes to preparing your tax returns, if you can’t tell the difference between me and the person at your church who is using Turbo Tax and charging $100 per return, we are both probably better off if you choose that person, me for the long-term health of my business and you, well, until you aren’t.

#fullambo out

That’s me in super sneaky spy mode.

At the end of the day yesterday I was mailing some paperwork to a couple of clients (yes, we still do that here, especially for clients with limited internet access). I had to create mailing labels for the envelopes. We have a dedicated label printer to help with that job. When I upgraded the office computers this December, I also very carefully went through and updated firmware, drivers, and software for all of our peripheral devices including the label printer. Well, wouldn’t you know the label printer has new software. Software that wants to connect to MS Outlook 365. I hit the connect button and then it asked for my login information to MS Office 365. And then I stopped. Why? Because I had to give that a think:

- When I connect my Office 365 account to the vendor software for the label maker, just how much access are they getting?

- Do I trust that they are only going to use information within Outlook itself or by entering my MS Office 365 credentials do they have tentacles into my other Office applications as well?

- Even if I trusted that the “connect” software was only looking at the Outlook contact information, do I have any idea what the vendor is doing with that data or their requirements to keep it private?

I had no answers to these questions. Still don’t. So, while it’s an order of magnitude less convenient for me, until I can find answers or a workaround where I can control who’s doing what with the data, we’re typing each label for printing. Here’s why…

Every paid tax preparer has to have a written information security plan (or WISP). It describes our security protocols and our processes in the event of a data breach, unauthorized disclosure, or disaster. #Taxpros reading this, yes, your WISP needs to include disaster recovery provisions in addition to data breach and disclosure. Data breach (hacking, etc.) and unauthorized disclosure are two different dogs. Paid tax return preparers are required to obtain specific consent for certain disclosures of their clients’ information. Many, possibly most, #taxpros think of this as needing consent to talk to the parents of an independent adult child about that child’s taxes (when they are paying for return prep) or for talking with a client’s financial advisor to optimize their retirement account withdrawals or for providing a copy of a tax return to a mortgage broker. But there’s more to it than that.

Any time a paid preparer discloses private (not necessarily sensitive, not necessarily confidential) client information to another party they are supposed to have specific consent. Of course there are exceptions, return preparation software being the most obvious. I did not include my label machine’s vendor in my client consents for this year. I did ask for specific consent for my scheduling application, my mass e-mailing software, my client management software, my billing software, the application I used to send texts to clients, etc. Why? Because that’s what I’m required to do. And, yes, I think to an extent it is overkill. I think the IRS is way behind the times with respect to understanding just how automated and how connected tax office operations have become. I did my best to ensure that I was complying with the spirit of the IRS requirements without getting my office and my clients so bogged down in authorization paperwork that no time was left over to actually prepare tax returns. I took a hard look at the software subscriptions I was using to automate my practice and was careful to only include in each of them that client information that was absolutely necessary (for example, the mass e-mailing software only has e-mail addresses, no physical addresses or phone numbers, the texting software only has phone numbers and birthdates for sending birthday texts). I didn’t just create a spreadsheet from my tax software or Outlook and import that into each application.

Why am I telling you all of this? Because my social media is filled with tax professionals (new and experienced) who are using automation tools (and their cell phones) in their practices. And it is becoming clear to me just how many are only looking at convenience and not security. The vibe I’m getting is something along the lines of “well everyone else is doing it so it must be OK/safe.” It really isn’t. Security and convenience are always a balancing act. Some things at Tax Therapy are more difficult (or more manual) than they have to be because I have thought through the security consequences and decided to err on the side of a bit more manual processing. If your #taxpro has given it some thought and decided that they can accept or mitigate the potential risks of a given technology, that’s fine. Every practice is different and has different resources to devote to IT, software evaluation, etc. It’s all of those #taxpros who aren’t even giving the security side a second thought that I’m concerned about. And if you’re a taxpayer using a paid preparer, you should be too.

Paid tax return preparers are not allowed to sell your data. But what happens when they provide your data without your specific consent to a vendor who then sells it or uses it to sell you more products? I’m looking at you, Intuit! I’ve been reading that clients of preparers who use Intuit’s suite of professional products are being solicited to use one of Intuit’s DIY products when they sign in to, for example, retrieve their W2s and 1099s or complete their tax professional’s annual client organizer. Not cool. Not cool at all.

I can’t run my office profitably without a certain degree of automation. There’s only so many days in tax season, only so many hours in a day, and only so much brain time in a given set of hours. But Tax Therapy clients can rest assured that I have devoted a huge portion of my (not inconsequential) brain power to ensuring that I’m only disclosing as much of their data as I absolutely have to to a given vendor and that I am getting their consent to do so each year. Tax professionals, what about your office? Taxpayers, what about your #taxpro?

The CARES Act and the more recent legislation (it doesn’t have a catchy name so I’ll call it CARES2) have created an above-the-line adjustment for certain charitable contributions. Pro-tip: If it’s “above the (AGI) line” it’s an adjustment to income; if it’s below the (AGI) line it is a deduction. If you are a #taxpro reading this it’s important to use the correct language. If you’re a taxpayer reading this the tax outcomes are largely the same but I like to use the right language.

The CARES Act and the more recent legislation (it doesn’t have a catchy name so I’ll call it CARES2) have created an above-the-line adjustment for certain charitable contributions. Pro-tip: If it’s “above the (AGI) line” it’s an adjustment to income; if it’s below the (AGI) line it is a deduction. If you are a #taxpro reading this it’s important to use the correct language. If you’re a taxpayer reading this the tax outcomes are largely the same but I like to use the right language.

For Tax Year 2020 taxpayers who take the standard deduction can make an above-the-line adjustment for cash contributions of up to $300 on their 1040s. There’s a marriage penalty here. The $300 for 2020 is on a per return, not a per taxpayer basis. So single filers can make a $300 adjustment and married taxpayers filing a joint return can make a $300 adjustment. The IRS has recently issued guidance (that contradicts the actual law) that says married taxpayers filing separately can only take a $150 adjustment. It’s incorrect but the tax savings are not worth the expense if the IRS decides to assess a penalty (more on that later).

In the more recently passed legislation the marriage penalty was removed. Each taxpayer may contribute up to $300 in cash to qualified charitable organizations. So for Tax Year 2021 it is possible to take an up to $600 above the line adjustment on a jointly filed return. Singles and Heads of Household still can take up to $300. Again, this is for taxpayers who do not itemize their deductions. Taxpayers who use Schedule A to itemize their deductions continue to deduct all of their qualified contributions on that schedule.

Now for the fine print. The IRS will be watching. The Service has stated that there will be a 50% penalty if you claim this adjustment without proper substantiation. What does that mean? It means receipts. Here’s a link to some information on proper recordkeeping for charitable contributions. In general, clients should always be maintaining the records necessary to substantiate their charitable contributions. But for this adjustment in particular it is even more important for the #taxpro to keep the receipts that substantiate this adjustment in the client’s tax file for the applicable years in case the IRS comes looking for them. Don’t be the client who tells your #taxpro “just take the max.” And if you are a #taxpro who “just takes the max” without proper substantiation then you aren’t really a #taxpro in my opinion. True tax professionals do not open their clients up to these types of penalties. They are too easily avoided. If you don’t have the proper documentation it’s going to cost you more in penalties than you saved in taxes by taking an unsubstantiated adjustment. Just don’t do it.

Remember, this adjustment has the following conditions:

- The taxpayer must not be itemizing their deductions on the return.

- The taxpayer must be able to substantiate the deduction.

- The contribution must be made in cash or a cash equivalent (cash, check, credit card, etc.). In other words it can’t be taken for donated “stuff”.

- The contribution must be made to a qualified charitable organization. Shorthand for that is that it must be made to a recognized 501(c)(3) organization.

See that last bit? It’s important to understand that not every tax exempt organization is a recognized 501(c)(3) organization.

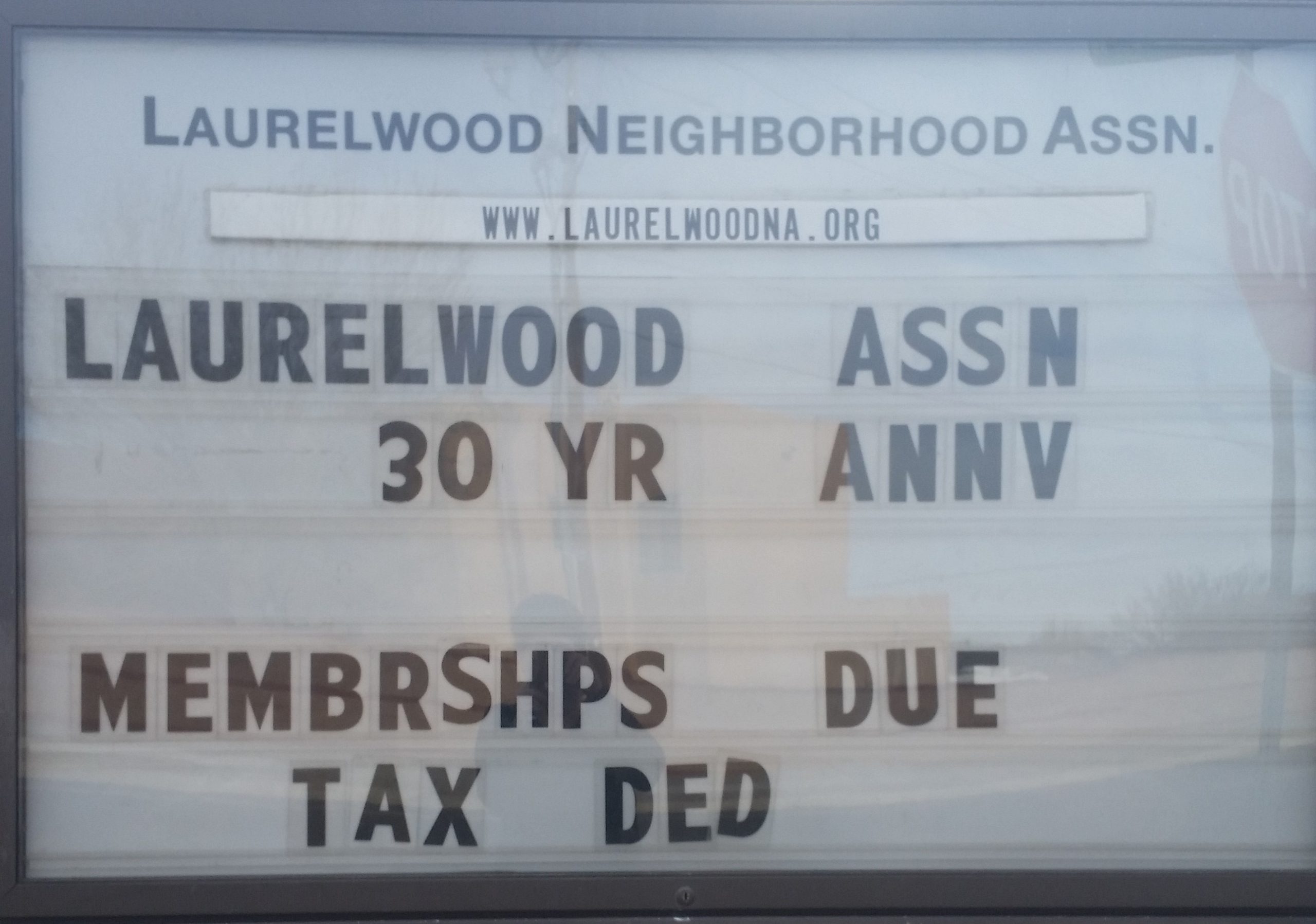

I saw this sign as I was driving home a while ago and thought “Yikes!” Your neighborhood association dues, homeowners association dues, and many other payments or contributions to tax exempt organizations are not tax deductible. Raffle tickets and purchases of auction items are also not deductible, no matter how worthy the cause.* Neither are contributions made to individuals (via gofundme or other types of crowdfunding) or contributions made to charitable organizations outside the U.S. (again, to be deductible the organization must be a 501(c)(3)).

I saw this sign as I was driving home a while ago and thought “Yikes!” Your neighborhood association dues, homeowners association dues, and many other payments or contributions to tax exempt organizations are not tax deductible. Raffle tickets and purchases of auction items are also not deductible, no matter how worthy the cause.* Neither are contributions made to individuals (via gofundme or other types of crowdfunding) or contributions made to charitable organizations outside the U.S. (again, to be deductible the organization must be a 501(c)(3)).

If you have questions about whether or not your contribution is deductible it’s always better to ask your #taxpro or to look to reliable sources for more information. Reliable sources include the tax team at Forbes.com, the IRS website, and (sometimes) the knowledge base provided by your DIY software vendor. Reliable sources do not include TikTok, Twitter, or YouTube unless the person providing the advice is recognized as an expert in the field (again, the IRS, Forbes, etc.). And occasionally even trustworthy sources provide incorrect information. Right now information is changing so quickly what you are reading could already be obsolete. Be careful out there. Read the fine print and remember, if it sounds too good to be true it usually is.

#fullambo out

*If you paid substantially more than fair market value for an auction item you may be able to deduct the amount in excess of fair market value but be prepared to answer some questions and provide some proof to your tax professional.

We’re not quite to the new year yet, but I’m sprinting toward the goal line!

I’m also expecting that many taxpayers will be required to complete a new Form W4 soon. Form W4 is what your employer uses to determine how much federal and state income tax to withhold from your paycheck each pay period. It contains basic information such as your name, address and taxpayer ID number (usually your SSN). The old form used to ask you to calculate how many “allowances” or “exemptions” from withholding you wanted to claim. And there was a worksheet. The higher the number of allowances the lower the withholding. So, to have the maximum amount withheld you simply claimed “Single 0.” The new form doesn’t work that way. On the surface it looks more complex than the old form but my colleague, Sherrell Martin, has done this amazing video that shows that the new form is actually pretty easy to complete and she walks you through how to complete it!

I’m also expecting that many taxpayers will be required to complete a new Form W4 soon. Form W4 is what your employer uses to determine how much federal and state income tax to withhold from your paycheck each pay period. It contains basic information such as your name, address and taxpayer ID number (usually your SSN). The old form used to ask you to calculate how many “allowances” or “exemptions” from withholding you wanted to claim. And there was a worksheet. The higher the number of allowances the lower the withholding. So, to have the maximum amount withheld you simply claimed “Single 0.” The new form doesn’t work that way. On the surface it looks more complex than the old form but my colleague, Sherrell Martin, has done this amazing video that shows that the new form is actually pretty easy to complete and she walks you through how to complete it!

If you are going to use the video to complete your new W4 it will be helpful to first gather the following information:

- The annual salary/salaries for you and your spouse for each of your jobs

- The number of pay periods per job

- The number of children and other dependents that will be claimed on your tax return*

- The amount of your itemized deductions (if you are not taking the standard deduction)*

*This information can be easily found on the comparison worksheet included with your tax return. My clients can find their “comp sheet” toward the top of the left hand pocket of their tax folder (or near the top of their PDF return copy). Even if you don’t use a paid tax preparer, most DIY software provides a comp sheet.

So, gather your information and let Sherrell walk you through the process of completing your new W4. Remember this new W4 and the associated withholding tables are designed to have you withholding the most accurate amount of tax, not the amount that will get you a big refund. You could even end up with a balance due when you file your tax return.

At Tax Therapy we include a mid-year withholding check up with our full-service return preparation. We will do a basic estimate of your annual income, credits, deductions, and withholding to determine if you need to make any adjustments for the rest of the year. And, while helping clients complete a new W4 is not included with tax return preparation, we can help you do that for an additional fee. If you are interested please log into your TaxDome account using the link in the Client Resources tab and send us a message.

Remember when they were doing direct deposit or mailing a paper check? Well someone convinced someone that prepaid debit cards were a better idea. I won’t wax philosophical on the fact that you can’t usually pay rent with a debit card. Instead, I will link to this article from The Tax Girl letting you know that debit card is legit…so don’t throw it away!

Remember when I talked about college students who are dependents (or basically any child over 16) not being eligible for the dependent EIP or their own EIP? Well, that applies to adult dependents too. So if you’re claiming your parent as a dependent and they are wondering where their stimulus money is—it isn’t coming. Because they are a dependent over the age of 16. Yeah—this is a drag.

What’s not a drag is that I have been moving through the returns and Cat may be coming back part time starting next week. Can I get a hallelujah?!

And we are open by appointment for document drop off, return review and signature, and for new client intake appointments.

That’s about it for today!

Wow! That’s all I can say. This blog post is late because I have managed to string together three productive work days in a row and it feels like it’s gonna hold through the rest of the week!

Wow! That’s all I can say. This blog post is late because I have managed to string together three productive work days in a row and it feels like it’s gonna hold through the rest of the week!

So, where are we at? Unfortunately we are still in early to mid-March as far as return processing goes. That said, Cat is coming to pick up the last pile of returns for scanning this week and I am moving through the piles. I am still fiddling with some of the more complicated returns but I’m working on those in tandem with some of the more straightforward ones. The short version is, returns are getting finished.

This is the first time this year I have felt like tax season is working. The first time I have felt like it’s actually tax season and things are working the way they are supposed to—stacked up but moving.

I will be working on returns the rest of this week and back in and working next week as well. I don’t have Cat available for data entry right now (she can’t do that from home) but if you’ve been with me any length of time you know how fast I type. I’ll get ’em done. Have a great week and enjoy the weekend.

#fullambo out

In case you missed the memo, NM Governor Michelle Lujan Grisham (a.k.a. Notorious MLG), has extended the stay-at-home order through May 15th. Cat and I are going to continue to honor that by Cat staying at home. That means no phone support for me. That means leave a message! I am usually at the office (although I will admit that “gardener’s hours” are starting to kick in) and I stop work to pick up phone messages a few times a day.

In case you missed the memo, NM Governor Michelle Lujan Grisham (a.k.a. Notorious MLG), has extended the stay-at-home order through May 15th. Cat and I are going to continue to honor that by Cat staying at home. That means no phone support for me. That means leave a message! I am usually at the office (although I will admit that “gardener’s hours” are starting to kick in) and I stop work to pick up phone messages a few times a day.

The backlog is slowly clearing. That means, for those of you whose returns still haven’t made it into the office, we will be ready to start accepting new paperwork soon. So here’s the plan—

Whether or not the stay-at-home is extended beyond May 15th, I will re-open the office for document drop offs by appointment only on Tuesday, May 19th. My 24th wedding anniversary is Monday the 18th so I’ll probably take that day off. If you wish to make an appointment to drop off your tax return documents or missing paperwork (K1s, corrected broker 1099s, etc.), please just call or e-mail and I or Cat will get back to you and will set you up!

I will probably re-open the office to new clients at the beginning of June. We will still be, to the greatest extent possible or required, limiting in-person visits to the office. Re-opening to new clients simply means that I will once again be accepting inquiries from new clients. So, if you know anyone who hasn’t filed but wants to, June is when I’ll be accepting referrals again. That should be plenty of time to meet the July 15th filing deadline.

Thanks to all of you for hanging in there through this chaotic tax season with me!

#fullambo out