This post is not about the different types of credentials for paid tax practitioners. You can read about that here. This post is about the difference between box fillers and true tax professionals. Even someone with letters can be a box filler instead of a true tax professional.

This post is not about the different types of credentials for paid tax practitioners. You can read about that here. This post is about the difference between box fillers and true tax professionals. Even someone with letters can be a box filler instead of a true tax professional.

If you are a taxpayer reading this I hope it gives you some insight into why some of us charge what we do, why some of us ask way more questions than your prior preparer did, and why some of us get really salty and give you a version of “don’t let the door hit you in the butt” when you tell us in March that someone at your church will do your taxes more cheaply and without all the questions.

If you are a tax practitioner (enrolled or unenrolled, full time or part time, self employed or employee) reading this I hope it makes you think about your professional obligations and what type of tax professional you currently are and what type you want to be. Again, not the letters, letters show a degree of dedication and seriousness, but aren’t a guarantee of passion for the profession or, sadly, competence.

I’ve been noticing certain entrepreneurial types selling practitioner education, especially for the EA credential (which requires a test but not a college degree or an apprenticeship period), by saying that once someone completes the training and/or passes the EA exam that they are ready to prepare tax returns and represent taxpayers before the IRS. They are not ready. They are especially not ready to open their own businesses (many have no idea about information security requirements, insurance, etc.). Now, I love the Enrolled Agent credential because it doesn’t present as many barriers to entry to the profession as, for example, the CPA credential. Too often these barriers to entry have been arbitrarily used to keep our profession old, white, and male. But the lack of barriers to entry is both a blessing and a curse.

Lately I’ve been tweeting about some of what I see in FaceBook groups for paid tax practitioners. Some (not all) of these practitioners are new EAs and they are now opening their own tax practices without any actual experience preparing tax returns. It’s awful. Truly awful. Not as bad as some of the advice being given by finance and business “influencers” on the various social media platforms (save me from Tik Tok Tax!), but still pretty bad. Here are a few examples:

- An investment adviser who does “a small amount of tax prep” asking other professionals how to set up accounting software.

- A brand new CPA with zero tax experience preparing returns for “friends & family” with zero awareness of the most basic knowledge needed to prepare a Schedule C (Profit/Loss from Business)

- Paid preparers telling other paid preparers who does and doesn’t qualify as a dependent without explaining the tests for “qualifying child” v “qualifying relative” or citing form instructions or any substantial authority

So what is the difference between a true tax professional and a box filler?

- True tax professionals know to consult the form instructions and/or a quick reference tool (which they are willing to purchase each year) before asking questions of other practitioners on social media. It always amazes me how many people who get paid to prepare tax returns clearly do not consult the form instructions when they have a question about an entry on a return.

- True tax professionals understand the concept of “substantial authority” when taking a position (even something as seemingly obvious as filing status or who qualifies as a dependent) on a tax return. IRS publications and what other people said on social media and googled articles may all be correct, but they are not authority. Tax practitioners need to be aware that there is actual “substantial authority” underlying the correct answers and know where to find it just in case the return is ever examined (audited).

- True tax professionals have a grasp of tax concepts beyond simply which amounts from which forms go on which lines of a tax return. They understand how the lines and forms are related to each other and the tax concepts (capital gains, passive income, business income & expense, etc.) underlying the mechanics of the return. Box fillers know mechanics (what goes where). True tax professionals can look at a tax return and spot items that look “wonky” and can (and will) go back into their software to investigate.

- True tax professionals do not rely on software to find errors or to prepare a return. They use it for automation and arithmetic. They know enough to be able to spot when the arithmetic might be wrong or when the return is not correct (i.e., something is being reported on the wrong line, form, or schedule).

- True tax professionals, even if they rarely consult the Internal Revenue Code (IRC), understand fundamental concepts in tax law such as gross income, business versus hobby, capital gains, etc. They may not be able to quote IRC “chapter and verse” (yet), but they have learned enough to have internalized the fundamentals.

- True tax professionals know what they don’t know and know when to refer a client or potential client to a specialist. For example, I know the basics of cryptocurrency taxation and if one of my clients decides to dabble, I’m pretty confident that I could prepare an accurate return. If, however, a serious crypto trader wanted to be my client, I would consult with the crypto specialists I know to determine what additional skills and software I should have before accepting this engagement. I might need to spend money to get the education and resources I need to take this client but that could also open the opportunity for more of the same type of client. If I’m not willing or able to spend the necessary money and time (maybe I just don’t want to do that kind of work) then I am ready to refer this client to someone who specializes.

All that said, many taxpayers only need a box filler. Single people with a few W2s and no children who could DIY but don’t want to do not necessarily need a true tax professional. The problem with choosing a box filler is that if life changes complicate the tax situation your box filler may not know how to prepare the return. And worse, the box filler may not know what they don’t know. Taxpayers should exercise caution when choosing someone to prepare their tax returns and anyone accepting payment for preparing a tax return needs to consider the harm they are doing to taxpayers and the professional preparer community when they work outside their competence level.

#fullambo out

The CARES Act and the more recent legislation (it doesn’t have a catchy name so I’ll call it CARES2) have created an above-the-line adjustment for certain charitable contributions. Pro-tip: If it’s “above the (AGI) line” it’s an adjustment to income; if it’s below the (AGI) line it is a deduction. If you are a #taxpro reading this it’s important to use the correct language. If you’re a taxpayer reading this the tax outcomes are largely the same but I like to use the right language.

The CARES Act and the more recent legislation (it doesn’t have a catchy name so I’ll call it CARES2) have created an above-the-line adjustment for certain charitable contributions. Pro-tip: If it’s “above the (AGI) line” it’s an adjustment to income; if it’s below the (AGI) line it is a deduction. If you are a #taxpro reading this it’s important to use the correct language. If you’re a taxpayer reading this the tax outcomes are largely the same but I like to use the right language.

For Tax Year 2020 taxpayers who take the standard deduction can make an above-the-line adjustment for cash contributions of up to $300 on their 1040s. There’s a marriage penalty here. The $300 for 2020 is on a per return, not a per taxpayer basis. So single filers can make a $300 adjustment and married taxpayers filing a joint return can make a $300 adjustment. The IRS has recently issued guidance (that contradicts the actual law) that says married taxpayers filing separately can only take a $150 adjustment. It’s incorrect but the tax savings are not worth the expense if the IRS decides to assess a penalty (more on that later).

In the more recently passed legislation the marriage penalty was removed. Each taxpayer may contribute up to $300 in cash to qualified charitable organizations. So for Tax Year 2021 it is possible to take an up to $600 above the line adjustment on a jointly filed return. Singles and Heads of Household still can take up to $300. Again, this is for taxpayers who do not itemize their deductions. Taxpayers who use Schedule A to itemize their deductions continue to deduct all of their qualified contributions on that schedule.

Now for the fine print. The IRS will be watching. The Service has stated that there will be a 50% penalty if you claim this adjustment without proper substantiation. What does that mean? It means receipts. Here’s a link to some information on proper recordkeeping for charitable contributions. In general, clients should always be maintaining the records necessary to substantiate their charitable contributions. But for this adjustment in particular it is even more important for the #taxpro to keep the receipts that substantiate this adjustment in the client’s tax file for the applicable years in case the IRS comes looking for them. Don’t be the client who tells your #taxpro “just take the max.” And if you are a #taxpro who “just takes the max” without proper substantiation then you aren’t really a #taxpro in my opinion. True tax professionals do not open their clients up to these types of penalties. They are too easily avoided. If you don’t have the proper documentation it’s going to cost you more in penalties than you saved in taxes by taking an unsubstantiated adjustment. Just don’t do it.

Remember, this adjustment has the following conditions:

- The taxpayer must not be itemizing their deductions on the return.

- The taxpayer must be able to substantiate the deduction.

- The contribution must be made in cash or a cash equivalent (cash, check, credit card, etc.). In other words it can’t be taken for donated “stuff”.

- The contribution must be made to a qualified charitable organization. Shorthand for that is that it must be made to a recognized 501(c)(3) organization.

See that last bit? It’s important to understand that not every tax exempt organization is a recognized 501(c)(3) organization.

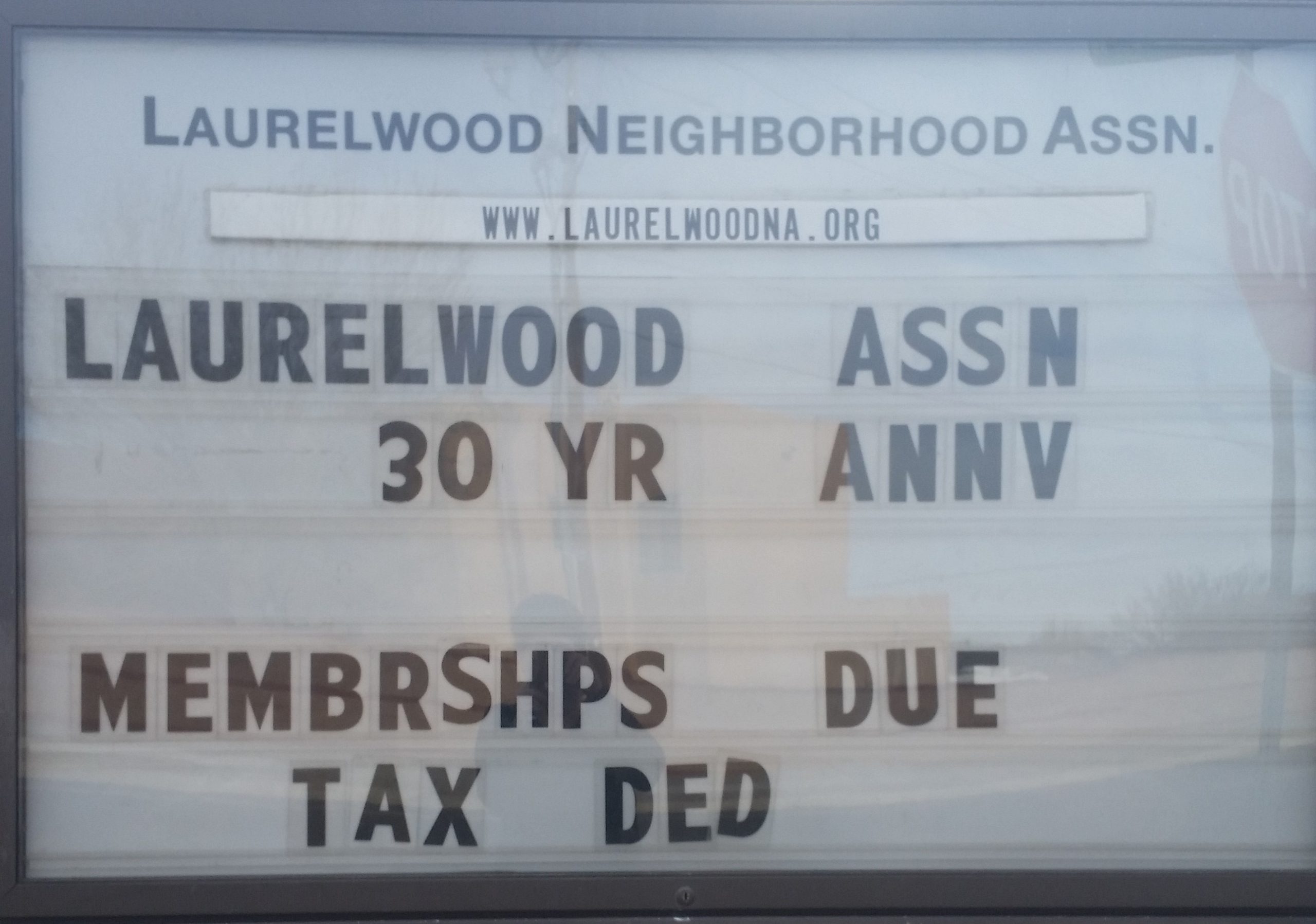

I saw this sign as I was driving home a while ago and thought “Yikes!” Your neighborhood association dues, homeowners association dues, and many other payments or contributions to tax exempt organizations are not tax deductible. Raffle tickets and purchases of auction items are also not deductible, no matter how worthy the cause.* Neither are contributions made to individuals (via gofundme or other types of crowdfunding) or contributions made to charitable organizations outside the U.S. (again, to be deductible the organization must be a 501(c)(3)).

I saw this sign as I was driving home a while ago and thought “Yikes!” Your neighborhood association dues, homeowners association dues, and many other payments or contributions to tax exempt organizations are not tax deductible. Raffle tickets and purchases of auction items are also not deductible, no matter how worthy the cause.* Neither are contributions made to individuals (via gofundme or other types of crowdfunding) or contributions made to charitable organizations outside the U.S. (again, to be deductible the organization must be a 501(c)(3)).

If you have questions about whether or not your contribution is deductible it’s always better to ask your #taxpro or to look to reliable sources for more information. Reliable sources include the tax team at Forbes.com, the IRS website, and (sometimes) the knowledge base provided by your DIY software vendor. Reliable sources do not include TikTok, Twitter, or YouTube unless the person providing the advice is recognized as an expert in the field (again, the IRS, Forbes, etc.). And occasionally even trustworthy sources provide incorrect information. Right now information is changing so quickly what you are reading could already be obsolete. Be careful out there. Read the fine print and remember, if it sounds too good to be true it usually is.

#fullambo out

*If you paid substantially more than fair market value for an auction item you may be able to deduct the amount in excess of fair market value but be prepared to answer some questions and provide some proof to your tax professional.

Remember when they were doing direct deposit or mailing a paper check? Well someone convinced someone that prepaid debit cards were a better idea. I won’t wax philosophical on the fact that you can’t usually pay rent with a debit card. Instead, I will link to this article from The Tax Girl letting you know that debit card is legit…so don’t throw it away!

Remember when I talked about college students who are dependents (or basically any child over 16) not being eligible for the dependent EIP or their own EIP? Well, that applies to adult dependents too. So if you’re claiming your parent as a dependent and they are wondering where their stimulus money is—it isn’t coming. Because they are a dependent over the age of 16. Yeah—this is a drag.

What’s not a drag is that I have been moving through the returns and Cat may be coming back part time starting next week. Can I get a hallelujah?!

And we are open by appointment for document drop off, return review and signature, and for new client intake appointments.

That’s about it for today!

Wow! That’s all I can say. This blog post is late because I have managed to string together three productive work days in a row and it feels like it’s gonna hold through the rest of the week!

Wow! That’s all I can say. This blog post is late because I have managed to string together three productive work days in a row and it feels like it’s gonna hold through the rest of the week!

So, where are we at? Unfortunately we are still in early to mid-March as far as return processing goes. That said, Cat is coming to pick up the last pile of returns for scanning this week and I am moving through the piles. I am still fiddling with some of the more complicated returns but I’m working on those in tandem with some of the more straightforward ones. The short version is, returns are getting finished.

This is the first time this year I have felt like tax season is working. The first time I have felt like it’s actually tax season and things are working the way they are supposed to—stacked up but moving.

I will be working on returns the rest of this week and back in and working next week as well. I don’t have Cat available for data entry right now (she can’t do that from home) but if you’ve been with me any length of time you know how fast I type. I’ll get ’em done. Have a great week and enjoy the weekend.

#fullambo out

In case you missed the memo, NM Governor Michelle Lujan Grisham (a.k.a. Notorious MLG), has extended the stay-at-home order through May 15th. Cat and I are going to continue to honor that by Cat staying at home. That means no phone support for me. That means leave a message! I am usually at the office (although I will admit that “gardener’s hours” are starting to kick in) and I stop work to pick up phone messages a few times a day.

In case you missed the memo, NM Governor Michelle Lujan Grisham (a.k.a. Notorious MLG), has extended the stay-at-home order through May 15th. Cat and I are going to continue to honor that by Cat staying at home. That means no phone support for me. That means leave a message! I am usually at the office (although I will admit that “gardener’s hours” are starting to kick in) and I stop work to pick up phone messages a few times a day.

The backlog is slowly clearing. That means, for those of you whose returns still haven’t made it into the office, we will be ready to start accepting new paperwork soon. So here’s the plan—

Whether or not the stay-at-home is extended beyond May 15th, I will re-open the office for document drop offs by appointment only on Tuesday, May 19th. My 24th wedding anniversary is Monday the 18th so I’ll probably take that day off. If you wish to make an appointment to drop off your tax return documents or missing paperwork (K1s, corrected broker 1099s, etc.), please just call or e-mail and I or Cat will get back to you and will set you up!

I will probably re-open the office to new clients at the beginning of June. We will still be, to the greatest extent possible or required, limiting in-person visits to the office. Re-opening to new clients simply means that I will once again be accepting inquiries from new clients. So, if you know anyone who hasn’t filed but wants to, June is when I’ll be accepting referrals again. That should be plenty of time to meet the July 15th filing deadline.

Thanks to all of you for hanging in there through this chaotic tax season with me!

#fullambo out

Economic Impact Payments

I got mine. So I can answer one question—no, the IRS is not going to “do the math” to see if your dependent child who was eligible for the Child Tax Credit (CTC) in 2018 or 2019 is going to be eligible in 2020. You will get the additional $500 payment if the child was CTC eligible (age 16 or under) on your most recently filed return. Every now and then my procrastination pays off. I’m pretty sure I’ll be filing my personal 1040 on July 14th.

I got mine. So I can answer one question—no, the IRS is not going to “do the math” to see if your dependent child who was eligible for the Child Tax Credit (CTC) in 2018 or 2019 is going to be eligible in 2020. You will get the additional $500 payment if the child was CTC eligible (age 16 or under) on your most recently filed return. Every now and then my procrastination pays off. I’m pretty sure I’ll be filing my personal 1040 on July 14th.

Moving forward, and I am advising individual clients as their returns are prepared, I will be either filing immediately or recommending that you wait until you receive your Economic Impact Payment (EIP or ‘stimulus check’) to file your 2019 return. The recommendation will be based on whatever is most advantageous for you. I have already advised some clients whose income was higher in 2019 than it was in 2018 to wait to file their 2019 return until they receive their EIP. I’ll be doing the same for clients with kids who were 16 in 2018. It’s called “tax planning” and it’s one of the reasons you pay a #taxpro.

Non-filers (you aren’t required to file a return, not that you simply haven’t filed a return)

If you aren’t a client, or if you are a former client who dropped below the threshold for having to file a return, you have a couple of options depending on your individual circumstances:

- If you receive Social Security payments your EIP will be automatic. You will receive a direct deposit or a check without having to take any additional steps.

- If you don’t receive Social Security payments but you get, for example, SSI or VA payments and are still not required to file a return the IRS is providing a tool for you to enter the information necessary for you to receive your EIP.

It is important to remember that you should, under no circumstances, have to pay to receive your EIP. For best results always start at irs.gov or irs.gov/coronavirus, not Google. And watch out for phone calls and e-mails phishing for information as well. The scammers are out in force on this one.

Filers Who May Not Have Direct Deposit Information on File or Want to Update Their Direct Deposit information

According to Kelly Phillips Erb (aka The Tax Girl) in this Forbes article, the Treasury Department has created a new web tool for filers of 2018 or 2019 tax returns to input or update their direct deposit information (a whole two days before the #taxpro community expected it!). This tool can be used if you normally don’t get a refund, but rather, have to pay the IRS each tax season. You can use this tool to verify the amount of your EIP, confirm whether it will be direct deposit or check, and (if you are getting a paper check) enter direct deposit information to receive your payment more quickly as long as your check hasn’t already been mailed. Paper checks aren’t supposed to start being mailed until the end of this month or early May according to my most recent reading. You can also update your direct deposit information if your deposit isn’t already pending.

You need to have your most recently filed tax return in hand to answer some of the questions. If I prepared your return it is likely that the information the tool will be requesting will be on your COMPARE sheet (that handy three-year comparison that is usually at or near the top of the left-hand pocket of your tax folder).

Update! Word on the street (OK, on #TaxTwitter) is that the tool is not working correctly. Especially if you have not filed a 2019 return. Please be patient and check back once or twice a day. They will get it running eventually. Or I’ll post that they’ve scrapped it.

Finally, according to The Tax Girl:

For security reasons, the IRS plans to mail a letter about the economic impact payment to your last known address within 15 days after the payment is paid. The letter will provide information on how the payment was made and how to report any failure to receive the payment.

Based on my reading there are a host of complicating factors for economically vulnerable taxpayers, taxpayers who file injured spouse claims (one taxpayer of a married filing joint couple owes back child support and the other doesn’t), divorced taxpayers, etc. I’m not going to go into the weeds on those. If you are interested, I highly recommend the Procedurally Taxing Blog, but beware, the blog is written for tax attorneys and is not for the faint of heart. Nevertheless, several recent posts discuss some of the complicating factors in mostly plain language.

And that, taxpayers, is all I have to say about that. So, moving on…

Deadlines

As I already reported, the filing and payment deadline has been extended to July 15th. Pretty much all of the deadlines significant to my practice (including those for filing Tax Court petitions) have been extended. If you have to file an FBAR you have an automatic extension until October 15th. The good news is that the IRS recently clarified that the July 15th deadline specifically applied to taxpayers required to file a Form 8938 (for certain taxpayers with foreign bank account balances). Estate income tax returns as well as estate and gift wealth transfer tax returns have also, for the most part, been granted extended deadlines.

The one tiny bit that was still weird has also been fixed! All of the extensions resulted in Quarter 1 estimated tax payments being due after Quarter 2 payments were due. Until recently Quarter 1 payments were due on July 15th but Quarter 2 payments were still due on June 15th. That has been fixed. Now all balances due on 2019 returns as well as Quarter 1 and Quarter 2 estimated tax payments are due on July 15th (as of this writing). That’s good news and bad news. Yes, everyone has more time, but that does make it easier to forget about payments and to, perhaps, lose sight of just how much will be due in total on July 15, 2020. Consequently, I am encouraging all taxpayers with the means to do so to make their payments on time and/or to set calendar reminders with amounts due to ensure that those payments get made by the new deadline.

And speaking of payments…

Installment Agreements

If you are in an existing Installment Agreement with the IRS your payments have also been suspended. If you mail them a check, you can stop until July 15th. If you are in a direct debit agreement you need to contact your bank and ask them to suspend the payments temporarily. It is extremely important that you ensure that you direct the bank to reinstate your payments approximately two weeks before the first payment due after July 15th to ensure that you don’t default your agreement. I expect the IRS to be fairly graceful about this given the circumstances, but it’s always better not to count on that grace. And again, if the payments are not causing economic hardship, I certainly recommend that you continue to make them even though you don’t have to.

Student Loan Payments and Interest

One thing that I have not mentioned that was included in the CARES Act is that the Act suspends student loan payments through September 30, 2020. Both principal and interest payments are suspended with no penalty and no interest will accrue on these loans during the suspension period. So if making those payments is causing you a hardship, you can temporarily stop making them. Again, just don’t forget to start again when the suspension period ends!

That is what I know as of right now. The pace of legislation and the related relief provisions and the implementation guidance has slowed down a bit, especially for most of my clients. Larger firms and CPAs who handle larger small businesses are still getting hit pretty hard. Guidance concerning the Paycheck Protection Program loans (more on that in a future post) for partnerships and self-employed people just came out a day or two ago. I still expect that there will be more relief coming (including addressing the ‘donut hole’ for EIPs for college age dependents) but for now, the tax practitioner community is slowly catching up to the most recent batch of tax law changes and additional guidance.

Hang in there. Stay home. Stay healthy.

#fullambo out

When, where, how, I don’t know yet, but remember yesterday’s post where I mentioned the “donut hole” for college-age dependents? Two Michigan senators have introduced legislation to address that and it will probably be part of a larger Phase 4 relief package according to Kay Bell at Don’t Mess with Taxes.

This is me, showing you how to hold onto some of your money (or to mitigate the tax consequences of using it)…

Required Minimum Distributions (RMDs)

Recent legislation has suspended RMDs for 2020. If you haven’t already taken your RMD for 2020, you don’t have to. This includes RMDs from inherited IRAs.

You know what else got suspended? RMDs that were required by April 1, 2020 because the taxpayer turned 70.5 in 2019. Yep, so if you had to take your very first RMD in 2019, you actually had until April 1, 2020 to take it and now you don’t have to take it at all. Great if you happened to forget about it!

And remember, if you are turning 70.5 in 2020 your RMD age was increased to 72 (by the SECURE Act) so you don’t have a “first” RMD requirement this year. You take your first RMD by April 1 the year you turn 72.

But, Amber, what if I did take my RMD? Well, there might be some relief for you too. You have 60 days to roll that money back into your account or into an IRA (but you are only allowed one of these rollovers in a 12-month period, so be careful if you’ve done one recently). There’s a lot of fine print on this so it’s best to talk with either your investment adviser or an investment adviser you can trust. I happen to know one. Feel free to use the form on the home page or send me an e-mail if you would like his contact details. He can answer your questions, help you determine if you are eligible for the 60-day rollover, and can help you set up an IRA if you are allowed to put your funds back but maybe want a new account instead of, say, your employer’s 401(k).

Speaking of IRAs…

The deadline for making deductible contributions to your IRA has been extended to July 15, 2020 to coincide with the extended filing deadline. So if you haven’t filed your return yet you can still tweak your contribution (maybe contribute your Economic Impact Payment if you are sure you won’t need it). If you’ve already filed your return I expect you can still make an additional payment through July 15 and simply amend your return to reap the additional tax benefits. Please bear in mind that I have no official guidance on this specifically related to the CARES Act. It just seems logical that you would be able to amend your return to take advantage of the later contribution deadline. Remember, however, that amended returns must be filed on paper and if you use a paid preparer you will be charged for the work. You may even be charged more than you would save in taxes. It’s important to do the math. And it’s really important not to ask your #taxpro to do the math for you right now. I recommend waiting until at least mid-May to give us a chance to get through the returns on our desks (most of us are still working like the deadline wasn’t extended) and until some of this small business loan business has settled down (more on that in a future post).

I Need Money Now!

The CARES Act also provides some help if you need to take money out of your IRA or 401(k).

You can take out up to $100,000 from your IRA penalty free. Not tax free! But not subject to the 10% penalty for early withdrawal if you are under age 59.5. You can also include this income in three equal parts over three years instead of all in tax year 2020. That can help you use your money and stay in a lower tax bracket! And, in an unprecedented move, you also have three years to put some or all of that money back should your circumstances change.

If you are allowed to take a loan from your 401(k) the amount has been increased to a maximum of $100,000 (from $50,000). The due date for repayment has also been delayed for one year.

Please note that these must be “COVID-19 Related” distributions or loans. It is important to consult your IRA trustee/custodian (for an IRA distribution) or your company’s plan administrator and/or plan custodian (for 401(k) loans and distributions) to ensure that you meet the criteria for the distribution and to ensure you understand all of the requirements (the fine print). They can’t give advice on the tax consequences (how much to withhold, etc.) but they can tell you if you qualify for the COVID-19 distribution based on your specific circumstances and give other information related to your specific investments or plan. Finally, considering the state of the stock market right now, it may be best to avoid selling stocks that are in your retirement accounts right now. I mean, you want to buy low, sell high, not the other way around. So if you can avoid cashing out, it is probably best do try to ride this chaos out without selling low.

#fullambo out

OK. That may be understatement. I have never had to learn this much tax law on the fly and during the height of tax season. A tax season that, at least in my office, started woefully late. Many clients didn’t make getting their documents into the office a priority until “the virus issue” had already started. So—early March instead of mid- to late February. But my troubles are fixable. I and the taxpayers who count on me to file their returns have been granted more time. You know who hasn’t been granted more time? The IRS.

For all the piles of new information I am having to read, absorb, and analyze (and I have some of the best instructors in the country helping me with that, BTW), the IRS is having to read, absorb, analyze and implement. So are your state taxing authorities and unemployment departments. For some insight into what the IRS is experiencing, I’m going to recommend this article (it’s Part 1 of 2). I saw a post today from one of my favorite instructors (I call him Tax Yoda). He typically gives a ton of free time and help to other #taxpros during season answering complex questions and pointing people to where they should start their research. He was asking those #taxpros to ease up a bit. He’s trying to work on his clients’ returns, help create new classes based on the new law, answer calls and e-mails from clients about the new law and is still trying to help other tax professionals. But apparently he’s not doing that fast enough to suit some people. I’ve seen pleas on Twitter from NM Tax & Revenue and the NM Department of Workforce solutions that people please stop calling and e-mailing. They are working as fast as they can with extremely limited resources (people are working from home!) to implement the relief measures being passed by state and municipal governments. They need time and space to develop their forms and processes. They need some breathing time.

If you are a client of mine reading this I want to thank you from the bottom of my hard drive for your patience and for your silence. A manageable number of you have called or e-mailed with questions, but most of you are reading the Constant Contact updates and simply waiting for me to provide new information. I am so grateful. All of us are struggling right now and we are all in this together. Your kindness and patience are not going unnoticed. If you are not a client or if you are talking to other people who are talking about calling their #taxpro or the IRS or a state taxing authority, please encourage them to wait. Information will be provided as soon as it is available. Help is on the way but we all need to get out of the way of the people trying to provide it. So for now, hang on, hang in, and hang up.

#fullambo out.

I recently read that 95% of small businesses fail within the first 5 years due to either bad management, under capitalization, or some combination of the two. Tax issues for small business owners have the same roots. Bad record keeping is often a sign of bad management. Mileage is one of the most highly scrutinized and most common areas on which small businesses are examined (audited). If you are a small business owner who isn’t keeping good mileage records you may be leaving money on the table. Worse, if you are audited, legitimate business mileage expenses may be disallowed because of your failure to keep adequate records.

The Self Help tab of the Tax Therapy website (Get Organized and Get Answers) offers additional resources to help you track and substantiate your business mileage. In a nutshell, your business mileage log should be contemporaneous (done at about the same time or shortly after you make the drive) and should show the date of the trip, the business purpose of the trip, and the miles driven. It is really common for people to not record the business purpose of the trip on the mileage log. It’s a lot easier to do this when you record the miles than it is to try to re-build that from an appointment calendar!

Finally, a great way to record your starting and ending odometer readings for your annual mileage total is to take a picture of your odometer with your phone on January 1 and again on December 31. If you haven’t taken a picture of your odometer this year, it’s not too late. It won’t be perfect, but it will be close and it will help you get into a really good habit! I hope that one of your New Year’s Resolutions, if you are a small business owner, is to improve your record keeping! It’s easy to do once you make a habit of it. And it’s one of the simplest ways to make sure your start up stays up!