After almost a year, I’m back on the blog. Heading into the third pandemic-affected filing season, much has changed here at Tax Therapy.

First, I am working from home for the foreseeable future. That means the practice has transitioned from mostly office-based to mostly virtual. The only clients I will be seeing in person are those who qualify for a house call. I am still taking paper documents through the mail or, if you are in the Albuquerque area, by local courier. If you are a potential client please continue to browse the website and then, if you feel like I can meet your return preparation needs, click here to book a discovery call.

Second, I am (for the most part) now working solo. Cat has a new full-time job and will be helping as necessary to wrangle actual, and occasionally electronic, documents, but she will not be here to provide near instant answers to your phone calls and e-mails. Please allow 24-48 hours for a response and understand that during March it can take me up to 72 hours to respond to your inquiries.

Third, while I am currently accepting new clients, I am only accepting new 1040 clients (individual returns). I will not accept new clients who require entity returns (Forms 1065 or 1120-S) once filing season has started. Entity returns are much more complicated and the new client onboarding process is much too involved for one person working alone to attempt during tax season. Entity returns also have a March 15th deadline and I don’t feel that I can realistically meet that deadline for entity clients who are brand new in January. If you are interested in having me prepare your entity return, I encourage you to use the contact form to let me know and I will put you on a list of potential clients to contact later this year (typically starting in June).

Finally, my cutoff date for accepting new clients will likely be even earlier this year than it was last year. Last year I stopped accepting new clients on March 10th. This year I expect to stop accepting new clients as early as February 20th to ensure that I can manage my workload and meet the April 18th filing deadline for as many clients as possible. I have not yet decided whether or not I will be taking new clients during the summer and fall extension period. As Magic 8-ball says “signs point to no” but I reserve the right to change my mind.

Everyone (the IRS, the National Taxpayer Advocate, tax industry organizations, and tax professionals) are predicting another “hairy” filing season. Personally, I’m feeling a return to something resembling normal but I am also preparing for a bumpy ride. So put on your seatbelts and let’s get going!

This post is based on actual conversations that have occurred in the Tax Therapy office.

This post is based on actual conversations that have occurred in the Tax Therapy office.

Mid-March 2019. The phone rings and I answer it.

Me: Tax Therapy, this is Amber.

Caller: Hi, yes, I was wondering if you could do my taxes?

Me: Well we are taking new clients.

Caller: When can I get an appointment?

Me: Before I do that I need to let you know that we do not do taxes while you wait. Our process is to send you some preliminary paperwork to complete, have an intake appointment where we review the paperwork and your documents with you as well as doing an ID check, and then you leave your stuff and we put it into our processing queue and call you when it’s ready for review and signature. Right now the turnaround is about three weeks [2/3 of our volume came in during a 2 week period in March that year] but if you get onboarded I will make every effort to ensure that you are filed on time.

Caller: Oh. I really wanted to get them done right away.

Me: In that case I recommend using one of the large franchises, especially if you can find one that is locally owned and operated. They are set up for while you wait return processing. I am not.

Caller: I didn’t want to do that. I don’t like them and they are expensive.

Me: I’m sorry but I really don’t have anything else to offer you. Most of the smaller shops I know are either not taking new clients or fully booked right now.

Call ends.

Conversations like these happen all the time in small tax practices all across the country. When I’m helping tax practitioners with practice management I often tell them that managing client expectations is important. Equally important is communicating boundaries to potential clients.

This post is for taxpayers who may be shopping for a #taxpro for the first time or looking to make a change this filing season. The time to shop is now. Actually the time to shop was last fall, but most #taxpros aren’t thoroughly in the thick of things right now and can still accept new clients without requiring an extension.

If you are looking for a #taxpro it’s important to understand some of the realities of running a tax business.

First, it’s a business. In most cases your fee is not simply profit to us but is paying for things like software, insurance, and continuing education. Not to mention office rent, phone/internet, and staff. We cannot discount our fees because of your circumstances or expectations.

Overhead is a thing. Ever gone through a fast food drive through, purchased two full meals and thought “Wow. For a little more money I could have had better food and supported a local business.” When you purchase from a large franchise you are paying for convenience, consistency (which, like fast food, can still be hit or miss), and their overhead (physical space, employee training, and advertising). Small shops often have lower overhead but that doesn’t mean they have no overhead.

Tax season is, by its nature, time limited. In other words, there is a fixed amount of time to see clients. Many #taxpros factor this into their pricing. They figure they can do X number of returns in a season and need to make $ to cover their overhead and make a profit (in other words, actually pay themselves for the work they’re doing). Big franchises have some higher paid employees but also make use of armies of lower paid, lower experienced employees to maximize their profits (higher return volume, done for lower cost). In some big “fancy” firms your return may be reviewed and signed by a highly paid, highly experienced professional, but they may only be giving it a cursory review. Again, this helps firms increase their profits (which should be the goal of any business). In smaller shops, it’s often a highly experienced #taxpro actually working on your return with the help of some lower paid support staff. And there are only so many hours a day that we can “brain.”

If you’ve ever heard the phrase “good, fast, or cheap; pick any two” that applies. If you want personalized service and someone to take the time to listen to your calls and explain things to you, that is often not going to be your cheapest option. You may be able to find that level of service for a reasonable price (something in line with what a franchise would charge or maybe even a bit less due to lower overhead) but those firms are not going to be willing to adapt their business model to your expectations. In other words, they cannot change from a drop off firm to a while you wait firm because that is what you want. They are a drop off firm because that is how they both do their best work and because its factored into their price structure.

If you want while you wait service, expect to pay for it. Same thing if you want a highly personalized experience or need a lot of advice or want your #taxpro to be available year round.

If you’re looking for a lower price you may need to find a #taxpro who doesn’t maintain a physical office (rent is a huge part of overhead). No office may not guarantee a lower price, but if you need a #taxpro with a physical office space do not expect bargain basement prices. You may need to accept a longer turnaround time because they don’t have staff to help them. And having staff doesn’t guarantee fast turnaround (especially if the firm is already backlogged). Doing a thorough and accurate job on a tax return takes time, no matter how simple you may think your situation is. You may also need to accept that your #taxpro is only available during tax season and that you may not be able to find them if a situation arises May-December. Or that if you do find them, they may not have the time or experience needed to help you.

Finally, this is why #taxpros get really prickly mid season (OK, sometimes earlier) about price shoppers. Especially #taxpros in solo firms. At the height of tax season time spent on the phone with price shoppers is time that could be spent doing billable work.

Early April 2019 – Monday Morning

Cat was not working Saturday so I turned off the phone so I could focus on finishing returns. I worked a full 8-10 hour day. I either took Sunday off or spent it doing office administration or housework instead of working on tax returns. I get to the office and check the voicemail which includes a few inquiries from potential clients.

Me: Hi, this is Amber from Tax Therapy, I’m returning your call from Friday night.

Caller: Oh. I already found someone. You weren’t fast enough.

Me: OK. Great. Good luck and thanks for calling.

I think the caller expected me to feel bad. I did not. Again, my tax practice (and those of many other solo practitioners) are not set up to do high intake volume late in the season. I am well aware of my physical and mental limitations. There is a fixed amount of “deep work” I can do in a given day/week/filing season. By the time this caller called I was 90% focused on moving returns out of the office and doing “extension triage,” 5% focused on ongoing resolution matters for clients, and 5% focused on process improvements for next filing season. In other words, by the time this caller decided to look for a #taxpro, the current filing season was already all over but some shouting in my office. I still might have been accepting new clients, but not one whose turnaround expectations were so high. I mean, if the caller couldn’t wait until the next business day for me to return the call, what’s the likelihood of them accepting an extension?

The Final Word in Confusion

The big tax franchises and the DIY software providers spend a lot of resources convincing people that “every person is a tax person” and that return preparation is a transaction. A widget for sale. And the more widgets they sell the more profit they earn. When you’re looking for a smaller shop, before you start calling about price take some time to decide which type of shop you are really looking for. Do you want a high-volume transaction type shop or a smaller, more relationship oriented shop? Are you just looking for fast turnaround on a basic return or do you want more personal service? After you’ve answered those questions, then you can look at what’s available in your area and start price shopping. And again, be aware that if you’re calling during peak season many relationship shops may not be able to meet your expected turnaround time, may charge a higher price if they can meet it, and may not be taking new clients at all.

The CARES Act and the more recent legislation (it doesn’t have a catchy name so I’ll call it CARES2) have created an above-the-line adjustment for certain charitable contributions. Pro-tip: If it’s “above the (AGI) line” it’s an adjustment to income; if it’s below the (AGI) line it is a deduction. If you are a #taxpro reading this it’s important to use the correct language. If you’re a taxpayer reading this the tax outcomes are largely the same but I like to use the right language.

The CARES Act and the more recent legislation (it doesn’t have a catchy name so I’ll call it CARES2) have created an above-the-line adjustment for certain charitable contributions. Pro-tip: If it’s “above the (AGI) line” it’s an adjustment to income; if it’s below the (AGI) line it is a deduction. If you are a #taxpro reading this it’s important to use the correct language. If you’re a taxpayer reading this the tax outcomes are largely the same but I like to use the right language.

For Tax Year 2020 taxpayers who take the standard deduction can make an above-the-line adjustment for cash contributions of up to $300 on their 1040s. There’s a marriage penalty here. The $300 for 2020 is on a per return, not a per taxpayer basis. So single filers can make a $300 adjustment and married taxpayers filing a joint return can make a $300 adjustment. The IRS has recently issued guidance (that contradicts the actual law) that says married taxpayers filing separately can only take a $150 adjustment. It’s incorrect but the tax savings are not worth the expense if the IRS decides to assess a penalty (more on that later).

In the more recently passed legislation the marriage penalty was removed. Each taxpayer may contribute up to $300 in cash to qualified charitable organizations. So for Tax Year 2021 it is possible to take an up to $600 above the line adjustment on a jointly filed return. Singles and Heads of Household still can take up to $300. Again, this is for taxpayers who do not itemize their deductions. Taxpayers who use Schedule A to itemize their deductions continue to deduct all of their qualified contributions on that schedule.

Now for the fine print. The IRS will be watching. The Service has stated that there will be a 50% penalty if you claim this adjustment without proper substantiation. What does that mean? It means receipts. Here’s a link to some information on proper recordkeeping for charitable contributions. In general, clients should always be maintaining the records necessary to substantiate their charitable contributions. But for this adjustment in particular it is even more important for the #taxpro to keep the receipts that substantiate this adjustment in the client’s tax file for the applicable years in case the IRS comes looking for them. Don’t be the client who tells your #taxpro “just take the max.” And if you are a #taxpro who “just takes the max” without proper substantiation then you aren’t really a #taxpro in my opinion. True tax professionals do not open their clients up to these types of penalties. They are too easily avoided. If you don’t have the proper documentation it’s going to cost you more in penalties than you saved in taxes by taking an unsubstantiated adjustment. Just don’t do it.

Remember, this adjustment has the following conditions:

- The taxpayer must not be itemizing their deductions on the return.

- The taxpayer must be able to substantiate the deduction.

- The contribution must be made in cash or a cash equivalent (cash, check, credit card, etc.). In other words it can’t be taken for donated “stuff”.

- The contribution must be made to a qualified charitable organization. Shorthand for that is that it must be made to a recognized 501(c)(3) organization.

See that last bit? It’s important to understand that not every tax exempt organization is a recognized 501(c)(3) organization.

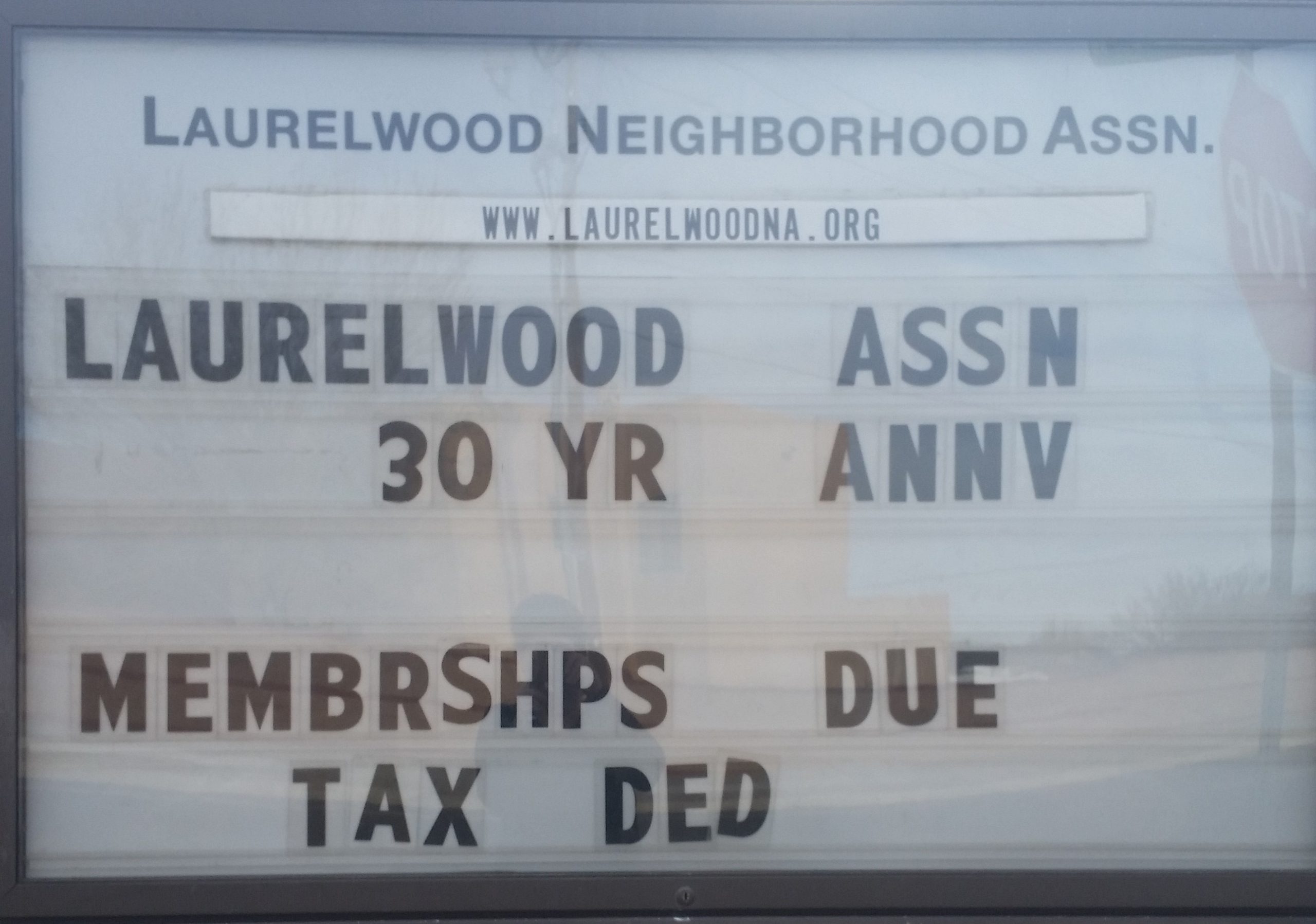

I saw this sign as I was driving home a while ago and thought “Yikes!” Your neighborhood association dues, homeowners association dues, and many other payments or contributions to tax exempt organizations are not tax deductible. Raffle tickets and purchases of auction items are also not deductible, no matter how worthy the cause.* Neither are contributions made to individuals (via gofundme or other types of crowdfunding) or contributions made to charitable organizations outside the U.S. (again, to be deductible the organization must be a 501(c)(3)).

I saw this sign as I was driving home a while ago and thought “Yikes!” Your neighborhood association dues, homeowners association dues, and many other payments or contributions to tax exempt organizations are not tax deductible. Raffle tickets and purchases of auction items are also not deductible, no matter how worthy the cause.* Neither are contributions made to individuals (via gofundme or other types of crowdfunding) or contributions made to charitable organizations outside the U.S. (again, to be deductible the organization must be a 501(c)(3)).

If you have questions about whether or not your contribution is deductible it’s always better to ask your #taxpro or to look to reliable sources for more information. Reliable sources include the tax team at Forbes.com, the IRS website, and (sometimes) the knowledge base provided by your DIY software vendor. Reliable sources do not include TikTok, Twitter, or YouTube unless the person providing the advice is recognized as an expert in the field (again, the IRS, Forbes, etc.). And occasionally even trustworthy sources provide incorrect information. Right now information is changing so quickly what you are reading could already be obsolete. Be careful out there. Read the fine print and remember, if it sounds too good to be true it usually is.

#fullambo out

*If you paid substantially more than fair market value for an auction item you may be able to deduct the amount in excess of fair market value but be prepared to answer some questions and provide some proof to your tax professional.

We’re not quite to the new year yet, but I’m sprinting toward the goal line!

I’m also expecting that many taxpayers will be required to complete a new Form W4 soon. Form W4 is what your employer uses to determine how much federal and state income tax to withhold from your paycheck each pay period. It contains basic information such as your name, address and taxpayer ID number (usually your SSN). The old form used to ask you to calculate how many “allowances” or “exemptions” from withholding you wanted to claim. And there was a worksheet. The higher the number of allowances the lower the withholding. So, to have the maximum amount withheld you simply claimed “Single 0.” The new form doesn’t work that way. On the surface it looks more complex than the old form but my colleague, Sherrell Martin, has done this amazing video that shows that the new form is actually pretty easy to complete and she walks you through how to complete it!

I’m also expecting that many taxpayers will be required to complete a new Form W4 soon. Form W4 is what your employer uses to determine how much federal and state income tax to withhold from your paycheck each pay period. It contains basic information such as your name, address and taxpayer ID number (usually your SSN). The old form used to ask you to calculate how many “allowances” or “exemptions” from withholding you wanted to claim. And there was a worksheet. The higher the number of allowances the lower the withholding. So, to have the maximum amount withheld you simply claimed “Single 0.” The new form doesn’t work that way. On the surface it looks more complex than the old form but my colleague, Sherrell Martin, has done this amazing video that shows that the new form is actually pretty easy to complete and she walks you through how to complete it!

If you are going to use the video to complete your new W4 it will be helpful to first gather the following information:

- The annual salary/salaries for you and your spouse for each of your jobs

- The number of pay periods per job

- The number of children and other dependents that will be claimed on your tax return*

- The amount of your itemized deductions (if you are not taking the standard deduction)*

*This information can be easily found on the comparison worksheet included with your tax return. My clients can find their “comp sheet” toward the top of the left hand pocket of their tax folder (or near the top of their PDF return copy). Even if you don’t use a paid tax preparer, most DIY software provides a comp sheet.

So, gather your information and let Sherrell walk you through the process of completing your new W4. Remember this new W4 and the associated withholding tables are designed to have you withholding the most accurate amount of tax, not the amount that will get you a big refund. You could even end up with a balance due when you file your tax return.

At Tax Therapy we include a mid-year withholding check up with our full-service return preparation. We will do a basic estimate of your annual income, credits, deductions, and withholding to determine if you need to make any adjustments for the rest of the year. And, while helping clients complete a new W4 is not included with tax return preparation, we can help you do that for an additional fee. If you are interested please log into your TaxDome account using the link in the Client Resources tab and send us a message.

Remember when they were doing direct deposit or mailing a paper check? Well someone convinced someone that prepaid debit cards were a better idea. I won’t wax philosophical on the fact that you can’t usually pay rent with a debit card. Instead, I will link to this article from The Tax Girl letting you know that debit card is legit…so don’t throw it away!

Remember when I talked about college students who are dependents (or basically any child over 16) not being eligible for the dependent EIP or their own EIP? Well, that applies to adult dependents too. So if you’re claiming your parent as a dependent and they are wondering where their stimulus money is—it isn’t coming. Because they are a dependent over the age of 16. Yeah—this is a drag.

What’s not a drag is that I have been moving through the returns and Cat may be coming back part time starting next week. Can I get a hallelujah?!

And we are open by appointment for document drop off, return review and signature, and for new client intake appointments.

That’s about it for today!

It’s Thursday and, after a fairly productive start to the week and a really hectic Wednesday, I am working from home. I have a 2-hour class today and I also needed to catch up on reading and administrative tasks.

The tax returns, however, keep on trucking. I’ll be back in the office tomorrow (Friday) working on returns. I’m still at the pile that came in in mid-March, which (if you have been keeping up with this blog) is most of them. But I’m finally seeing light at the end of the tunnel! I still expect to get most of the returns that normally would not have been on extension filed by the end of this month.

I am still planning on opening the office by appointment only beginning Tuesday afternoon, May 19th. I have already booked a few appointments so if you are wanting an appointment in May (and not in June) it’s best to call or e-mail and book now.

You can also call or e-mail if you are a client with a question about your Economic Impact Payment. I’ve been answering those as I can and I appreciate everyone’s understanding concerning the fact that while I have a lot of information on the process, I have absolutely no control over the IRS, the Treasury Department, or their tools (electronic or human).

I am still urging everyone to stay home to the greatest extent possible and to use e-mail, the phone, Zoom, the secure portal, or USPS/courier to communicate with me.

Enjoy your weekend everyone!

#fullambo out

Wow! That’s all I can say. This blog post is late because I have managed to string together three productive work days in a row and it feels like it’s gonna hold through the rest of the week!

Wow! That’s all I can say. This blog post is late because I have managed to string together three productive work days in a row and it feels like it’s gonna hold through the rest of the week!

So, where are we at? Unfortunately we are still in early to mid-March as far as return processing goes. That said, Cat is coming to pick up the last pile of returns for scanning this week and I am moving through the piles. I am still fiddling with some of the more complicated returns but I’m working on those in tandem with some of the more straightforward ones. The short version is, returns are getting finished.

This is the first time this year I have felt like tax season is working. The first time I have felt like it’s actually tax season and things are working the way they are supposed to—stacked up but moving.

I will be working on returns the rest of this week and back in and working next week as well. I don’t have Cat available for data entry right now (she can’t do that from home) but if you’ve been with me any length of time you know how fast I type. I’ll get ’em done. Have a great week and enjoy the weekend.

#fullambo out

OK! Still feeling like I’ve turned a corner. Getting returns processed. Cat is finding her “work at home” groove too. We are moving slowly through the stacks that have been here since mid-March when all hell broke loose. I am still having to set aside some of the more complex ones for when I am able to fully focus. When it comes to tax returns it’s a lot harder to fix them than it is to just get them right the first time. So I want to make sure I’m in top form when I’m working on the ones with a lot of moving parts (you know who you are).

If you still haven’t gotten your stuff into the office, that’s OK! Once I feel like most of the backlog has been cleared I will get a bit more pro-active about getting what remains out into the office. I’m hoping that this will roughly coincide with at least a lightening of some of the stay-at-home restrictions. We will see—that’s going to depend both on how quickly I work and how well we do at flattening the curve here in NM.

Again, we’ve got until July 15th and I’m planning on having most of them out well before then unless additional chaos ensues.

Thanks for hanging in there with us!

#fullambo out

Economic Impact Payments

I got mine. So I can answer one question—no, the IRS is not going to “do the math” to see if your dependent child who was eligible for the Child Tax Credit (CTC) in 2018 or 2019 is going to be eligible in 2020. You will get the additional $500 payment if the child was CTC eligible (age 16 or under) on your most recently filed return. Every now and then my procrastination pays off. I’m pretty sure I’ll be filing my personal 1040 on July 14th.

I got mine. So I can answer one question—no, the IRS is not going to “do the math” to see if your dependent child who was eligible for the Child Tax Credit (CTC) in 2018 or 2019 is going to be eligible in 2020. You will get the additional $500 payment if the child was CTC eligible (age 16 or under) on your most recently filed return. Every now and then my procrastination pays off. I’m pretty sure I’ll be filing my personal 1040 on July 14th.

Moving forward, and I am advising individual clients as their returns are prepared, I will be either filing immediately or recommending that you wait until you receive your Economic Impact Payment (EIP or ‘stimulus check’) to file your 2019 return. The recommendation will be based on whatever is most advantageous for you. I have already advised some clients whose income was higher in 2019 than it was in 2018 to wait to file their 2019 return until they receive their EIP. I’ll be doing the same for clients with kids who were 16 in 2018. It’s called “tax planning” and it’s one of the reasons you pay a #taxpro.

Non-filers (you aren’t required to file a return, not that you simply haven’t filed a return)

If you aren’t a client, or if you are a former client who dropped below the threshold for having to file a return, you have a couple of options depending on your individual circumstances:

- If you receive Social Security payments your EIP will be automatic. You will receive a direct deposit or a check without having to take any additional steps.

- If you don’t receive Social Security payments but you get, for example, SSI or VA payments and are still not required to file a return the IRS is providing a tool for you to enter the information necessary for you to receive your EIP.

It is important to remember that you should, under no circumstances, have to pay to receive your EIP. For best results always start at irs.gov or irs.gov/coronavirus, not Google. And watch out for phone calls and e-mails phishing for information as well. The scammers are out in force on this one.

Filers Who May Not Have Direct Deposit Information on File or Want to Update Their Direct Deposit information

According to Kelly Phillips Erb (aka The Tax Girl) in this Forbes article, the Treasury Department has created a new web tool for filers of 2018 or 2019 tax returns to input or update their direct deposit information (a whole two days before the #taxpro community expected it!). This tool can be used if you normally don’t get a refund, but rather, have to pay the IRS each tax season. You can use this tool to verify the amount of your EIP, confirm whether it will be direct deposit or check, and (if you are getting a paper check) enter direct deposit information to receive your payment more quickly as long as your check hasn’t already been mailed. Paper checks aren’t supposed to start being mailed until the end of this month or early May according to my most recent reading. You can also update your direct deposit information if your deposit isn’t already pending.

You need to have your most recently filed tax return in hand to answer some of the questions. If I prepared your return it is likely that the information the tool will be requesting will be on your COMPARE sheet (that handy three-year comparison that is usually at or near the top of the left-hand pocket of your tax folder).

Update! Word on the street (OK, on #TaxTwitter) is that the tool is not working correctly. Especially if you have not filed a 2019 return. Please be patient and check back once or twice a day. They will get it running eventually. Or I’ll post that they’ve scrapped it.

Finally, according to The Tax Girl:

For security reasons, the IRS plans to mail a letter about the economic impact payment to your last known address within 15 days after the payment is paid. The letter will provide information on how the payment was made and how to report any failure to receive the payment.

Based on my reading there are a host of complicating factors for economically vulnerable taxpayers, taxpayers who file injured spouse claims (one taxpayer of a married filing joint couple owes back child support and the other doesn’t), divorced taxpayers, etc. I’m not going to go into the weeds on those. If you are interested, I highly recommend the Procedurally Taxing Blog, but beware, the blog is written for tax attorneys and is not for the faint of heart. Nevertheless, several recent posts discuss some of the complicating factors in mostly plain language.

And that, taxpayers, is all I have to say about that. So, moving on…

Deadlines

As I already reported, the filing and payment deadline has been extended to July 15th. Pretty much all of the deadlines significant to my practice (including those for filing Tax Court petitions) have been extended. If you have to file an FBAR you have an automatic extension until October 15th. The good news is that the IRS recently clarified that the July 15th deadline specifically applied to taxpayers required to file a Form 8938 (for certain taxpayers with foreign bank account balances). Estate income tax returns as well as estate and gift wealth transfer tax returns have also, for the most part, been granted extended deadlines.

The one tiny bit that was still weird has also been fixed! All of the extensions resulted in Quarter 1 estimated tax payments being due after Quarter 2 payments were due. Until recently Quarter 1 payments were due on July 15th but Quarter 2 payments were still due on June 15th. That has been fixed. Now all balances due on 2019 returns as well as Quarter 1 and Quarter 2 estimated tax payments are due on July 15th (as of this writing). That’s good news and bad news. Yes, everyone has more time, but that does make it easier to forget about payments and to, perhaps, lose sight of just how much will be due in total on July 15, 2020. Consequently, I am encouraging all taxpayers with the means to do so to make their payments on time and/or to set calendar reminders with amounts due to ensure that those payments get made by the new deadline.

And speaking of payments…

Installment Agreements

If you are in an existing Installment Agreement with the IRS your payments have also been suspended. If you mail them a check, you can stop until July 15th. If you are in a direct debit agreement you need to contact your bank and ask them to suspend the payments temporarily. It is extremely important that you ensure that you direct the bank to reinstate your payments approximately two weeks before the first payment due after July 15th to ensure that you don’t default your agreement. I expect the IRS to be fairly graceful about this given the circumstances, but it’s always better not to count on that grace. And again, if the payments are not causing economic hardship, I certainly recommend that you continue to make them even though you don’t have to.

Student Loan Payments and Interest

One thing that I have not mentioned that was included in the CARES Act is that the Act suspends student loan payments through September 30, 2020. Both principal and interest payments are suspended with no penalty and no interest will accrue on these loans during the suspension period. So if making those payments is causing you a hardship, you can temporarily stop making them. Again, just don’t forget to start again when the suspension period ends!

That is what I know as of right now. The pace of legislation and the related relief provisions and the implementation guidance has slowed down a bit, especially for most of my clients. Larger firms and CPAs who handle larger small businesses are still getting hit pretty hard. Guidance concerning the Paycheck Protection Program loans (more on that in a future post) for partnerships and self-employed people just came out a day or two ago. I still expect that there will be more relief coming (including addressing the ‘donut hole’ for EIPs for college age dependents) but for now, the tax practitioner community is slowly catching up to the most recent batch of tax law changes and additional guidance.

Hang in there. Stay home. Stay healthy.

#fullambo out

This is me, showing you how to hold onto some of your money (or to mitigate the tax consequences of using it)…

Required Minimum Distributions (RMDs)

Recent legislation has suspended RMDs for 2020. If you haven’t already taken your RMD for 2020, you don’t have to. This includes RMDs from inherited IRAs.

You know what else got suspended? RMDs that were required by April 1, 2020 because the taxpayer turned 70.5 in 2019. Yep, so if you had to take your very first RMD in 2019, you actually had until April 1, 2020 to take it and now you don’t have to take it at all. Great if you happened to forget about it!

And remember, if you are turning 70.5 in 2020 your RMD age was increased to 72 (by the SECURE Act) so you don’t have a “first” RMD requirement this year. You take your first RMD by April 1 the year you turn 72.

But, Amber, what if I did take my RMD? Well, there might be some relief for you too. You have 60 days to roll that money back into your account or into an IRA (but you are only allowed one of these rollovers in a 12-month period, so be careful if you’ve done one recently). There’s a lot of fine print on this so it’s best to talk with either your investment adviser or an investment adviser you can trust. I happen to know one. Feel free to use the form on the home page or send me an e-mail if you would like his contact details. He can answer your questions, help you determine if you are eligible for the 60-day rollover, and can help you set up an IRA if you are allowed to put your funds back but maybe want a new account instead of, say, your employer’s 401(k).

Speaking of IRAs…

The deadline for making deductible contributions to your IRA has been extended to July 15, 2020 to coincide with the extended filing deadline. So if you haven’t filed your return yet you can still tweak your contribution (maybe contribute your Economic Impact Payment if you are sure you won’t need it). If you’ve already filed your return I expect you can still make an additional payment through July 15 and simply amend your return to reap the additional tax benefits. Please bear in mind that I have no official guidance on this specifically related to the CARES Act. It just seems logical that you would be able to amend your return to take advantage of the later contribution deadline. Remember, however, that amended returns must be filed on paper and if you use a paid preparer you will be charged for the work. You may even be charged more than you would save in taxes. It’s important to do the math. And it’s really important not to ask your #taxpro to do the math for you right now. I recommend waiting until at least mid-May to give us a chance to get through the returns on our desks (most of us are still working like the deadline wasn’t extended) and until some of this small business loan business has settled down (more on that in a future post).

I Need Money Now!

The CARES Act also provides some help if you need to take money out of your IRA or 401(k).

You can take out up to $100,000 from your IRA penalty free. Not tax free! But not subject to the 10% penalty for early withdrawal if you are under age 59.5. You can also include this income in three equal parts over three years instead of all in tax year 2020. That can help you use your money and stay in a lower tax bracket! And, in an unprecedented move, you also have three years to put some or all of that money back should your circumstances change.

If you are allowed to take a loan from your 401(k) the amount has been increased to a maximum of $100,000 (from $50,000). The due date for repayment has also been delayed for one year.

Please note that these must be “COVID-19 Related” distributions or loans. It is important to consult your IRA trustee/custodian (for an IRA distribution) or your company’s plan administrator and/or plan custodian (for 401(k) loans and distributions) to ensure that you meet the criteria for the distribution and to ensure you understand all of the requirements (the fine print). They can’t give advice on the tax consequences (how much to withhold, etc.) but they can tell you if you qualify for the COVID-19 distribution based on your specific circumstances and give other information related to your specific investments or plan. Finally, considering the state of the stock market right now, it may be best to avoid selling stocks that are in your retirement accounts right now. I mean, you want to buy low, sell high, not the other way around. So if you can avoid cashing out, it is probably best do try to ride this chaos out without selling low.

#fullambo out